In fintech, the Discovery stage goes far beyond outlining screens and user paths — it’s about proving that your product will function securely, perform reliably, and comply with every regulation the moment it enters the real world.

Each decision — from API selection to transaction architecture — can either support scalability or silently plant the seed for expensive rework.

Unlike in other industries, fintech Discovery determines not just what to build, but whether it’s even feasible within regulatory and technical boundaries. When done wrong, it leads to compliance risks, partner delays, or even complete product rewrites.

At Inspirit, we’ve seen too many fintech teams burn through months of work and tens of thousands of dollars simply because their Discovery phase missed a few crucial details. Here are the top five mistakes we see most often — and how to avoid them.

Many fintech founders treat payments, KYC, or banking rails as features they can connect later. But every integration has constraints — onboarding requirements, API rate limits, sandbox differences, and hidden compliance dependencies.

When you skip integration feasibility, you risk discovering too late that your chosen provider doesn’t support your use case or region.

What follows next: re-engineering, long approval cycles, and delays in revenue.

Our client expanding into Canada initially planned to integrate Interac after MVP launch. During Discovery, we uncovered specific transaction batch rules and asynchronous reconciliation requirements — issues that would’ve broken their entire payment flow. By addressing it early, we saved three months and a full redesign.

Map all critical integrations during the fintech Discovery stage.

Validate compliance prerequisites, transaction flow logic, and operational constraints before committing to a single architecture line.

In fintech, MVPs can’t be prototypes that “just validate ideas.” They must be stable, auditable, and compliant enough to gain trust from users and partners.

Yet many teams approach fintech Discovery with startup logic: minimal design, zero automation, no risk controls — and end up rebuilding everything after launch.

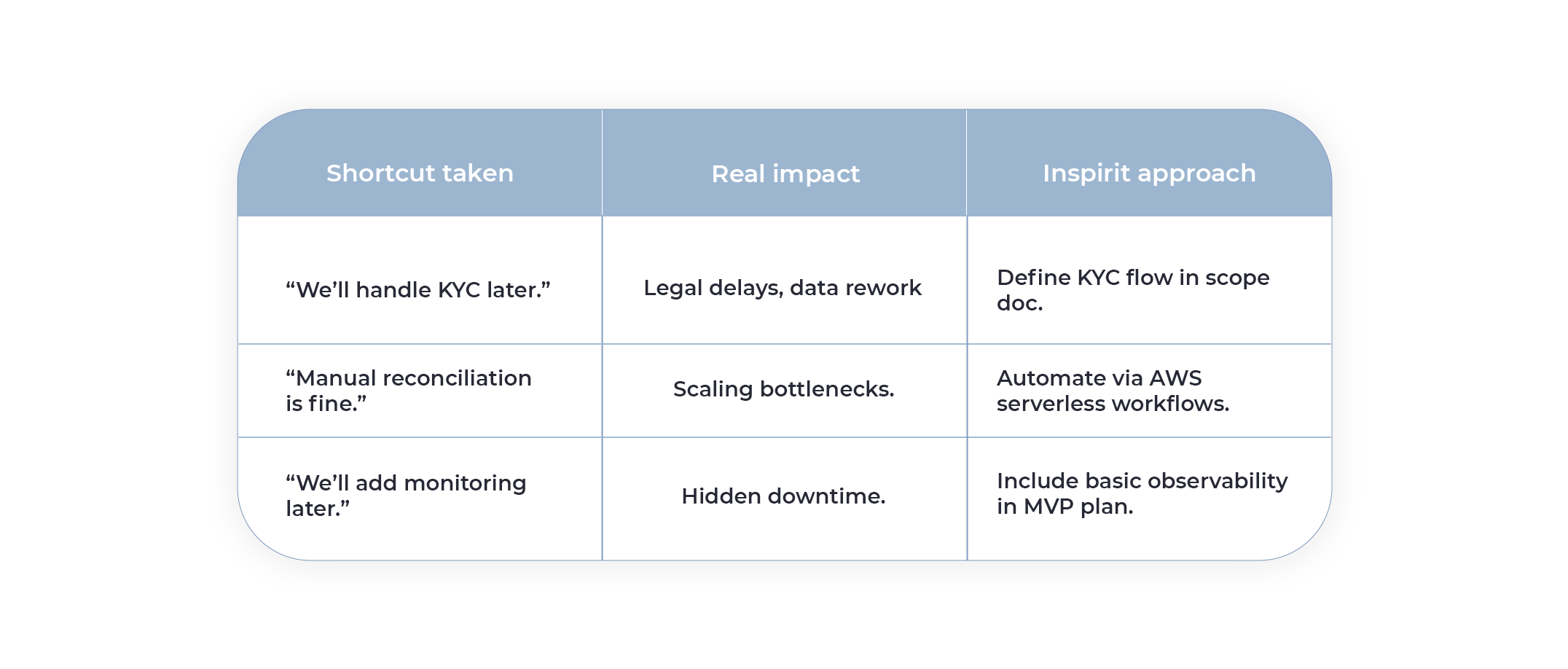

⬝ Skipped KYC logic = user data redesign later

⬝ No reconciliation = accounting overhead and audit failures

⬝ No observability = downtime without alerts

A fintech MVP should aim for minimum viable resilience, not just minimum viable features. We ensure Discovery defines a version of your product that can survive investor scrutiny and real banking partnerships — even in its first release.

Many Discovery phases end with static documents describing screens and flows — but no data modeling or performance baseline. In fintech, that’s a hidden trap.

When user or transaction volumes grow, systems designed without scalability in mind start breaking: slow responses, delayed settlements, rising cloud costs, and inconsistent reporting.

⬝ Transaction processing times that double under load. ⬝

⬝ Cloud bills rising 30–50% due to inefficient architecture.

⬝ Analytics pipelines rebuilt after launch because they weren’t designed for live data.

We treat performance as part of Discovery, not an afterthought. Then, we simulate data flow and stress conditions, define architecture patterns (like AWS event-driven microservices), and estimate real cost under load. This turns the fintech Discovery phase into a performance readiness check instead of a fancy design workshop.

Always include load scenarios and performance metrics in your Discovery deliverables. If they’re missing, your development budget is already underestimating future costs.

One of the most silent killers of fintech projects is a Discovery phase that produces beautiful documentation but no shared understanding between business and engineering teams.

When “business” speaks in features and “tech” speaks in dependencies, teams lose alignment quickly. This results in scope creep, missed priorities, and no one actually owning product decisions.

A business owner might think “we need document scanning,” while the technical team debates ML models, API costs, and latency — with no bridge in between.

We define each feature as a workflow with a business value, technical ownership, and risk category. This ensures every stakeholder — from CTO to product manager — sees exactly how a feature contributes to both business outcomes and technical integrity.

In the Spendbase project, defining “AI-driven check scanning” as an end-to-end workflow (not just a feature) clarified ownership between ML engineers and payment API devs. That structure prevented misaligned milestones and sped up delivery.

Discovery phases often end with one number: a “total project cost.” But in fintech, linear cost estimation (hours × rate) ignores uncertainty. Integrations change policies, compliance rules shift, and APIs get deprecated mid-build.

Underestimating these factors means your actual cost ends up 30–70% higher than expected — damaging investor trust and delaying launches.

We build a three-tier budget model inside every fintech Discovery:

1. Baseline – pure implementation, no surprises.

2. Risk Buffer – known fintech uncertainties (API delays, KYC reviews, regulation).

3. Optimization Scenario – cost reduction paths (reuse, automation, or prebuilt modules).

This model helps clients raise funds or allocate budgets with full awareness of both potential risks and savings.

A strong fintech Discovery produces real decisions — technical, operational, and financial — that guide your build with confidence.

⬝ Regulatory and market constraint analysis

⬝ Integration feasibility & compliance map

⬝ Scalable architecture blueprint with performance baselines

⬝ Risk-adjusted cost estimation

⬝ Ownership matrix for features and workflows

⬝ Roadmap from Discovery → Development

This process transforms vague ideas into precise implementation plans — so your development team can move fast without breaking compliance or burning budget.

Skipping the proper fintech Discovery phase doesn’t just cost money. It costs momentum. Every delayed integration, every late compliance fix, every “we didn’t expect that” moment pushes your launch further away and your investors closer to doubt.

Most fintech reworks we’ve rescued weren’t bad ideas — just misplanned ones. And in this industry, clarity is your most valuable currency.